Trump Accounts for Kids: What Every Parent Needs to Know in 2026

America’s newest savings program for children officially went live on July 4, 2026 — the same day the country celebrated its 250th birthday. Within days, more than six million families had already signed up. If you’re a parent, grandparent, or guardian and haven’t looked into this yet, here’s everything you need to know about Trump Accounts, how they work, and whether they’re worth opening for your child.

What Exactly Is a Trump Account?

A Trump Account is a new type of tax-advantaged investment account created for children under 18 who hold a valid Social Security number. Think of it as a retirement account that starts the day a child is born, rather than the day they get their first paycheck.

The accounts function much like a traditional IRA: money grows tax-deferred while the child is young, and once they turn 18, the account automatically converts into a regular traditional IRA under their own name and control.

Unlike a 529 plan, this money isn’t meant for college tuition or short-term expenses. It’s built for one purpose — long-term growth toward retirement, decades down the road.

Who Qualifies, and Who Gets Free Money?

Eligibility itself is simple: any child under 18 with a valid Social Security number can have an account opened for them by a parent, legal guardian, adult sibling, or grandparent.

But the free government seed money is more selective:

- $1,000 federal deposit — reserved for children born between January 1, 2025, and December 31, 2028. A parent or guardian must actively elect to receive it; it isn’t automatic.

- $250 charitable deposit — funded by a multi-billion-dollar pledge from a prominent foundation, available to children age 10 and under living in ZIP codes with median incomes at or below $150,000.

- Employer and philanthropic top-ups — dozens of major companies have pledged to match the $1,000 federal deposit for their employees’ kids, and several state-level philanthropic programs are adding their own contributions in select regions.

If your child doesn’t qualify for any seed money, you can still open an account and contribute on your own — you just won’t get the head start.

How Much Can You Contribute Each Year?

Once an account is open, family, friends, and even employers can chip in:

- $5,000 per year total contribution limit per child (indexed for inflation starting in later tax years)

- Employers can contribute up to $2,500 of that limit on an employee’s behalf, and it isn’t counted as taxable income

- Government seed deposits and qualifying charitable contributions don’t count against this annual cap

Where Does the Money Actually Go?

This isn’t a savings account sitting in cash — it’s invested. The default option for every new account is a low-cost S&P 500 index fund, with an expense ratio of just 0.02%. Down the line, families will get the choice to spread contributions across a handful of similar broad-market stock funds.

The accounts themselves are held and managed through a major online brokerage platform in partnership with a large custodial bank, both selected to run the program in its early phase.

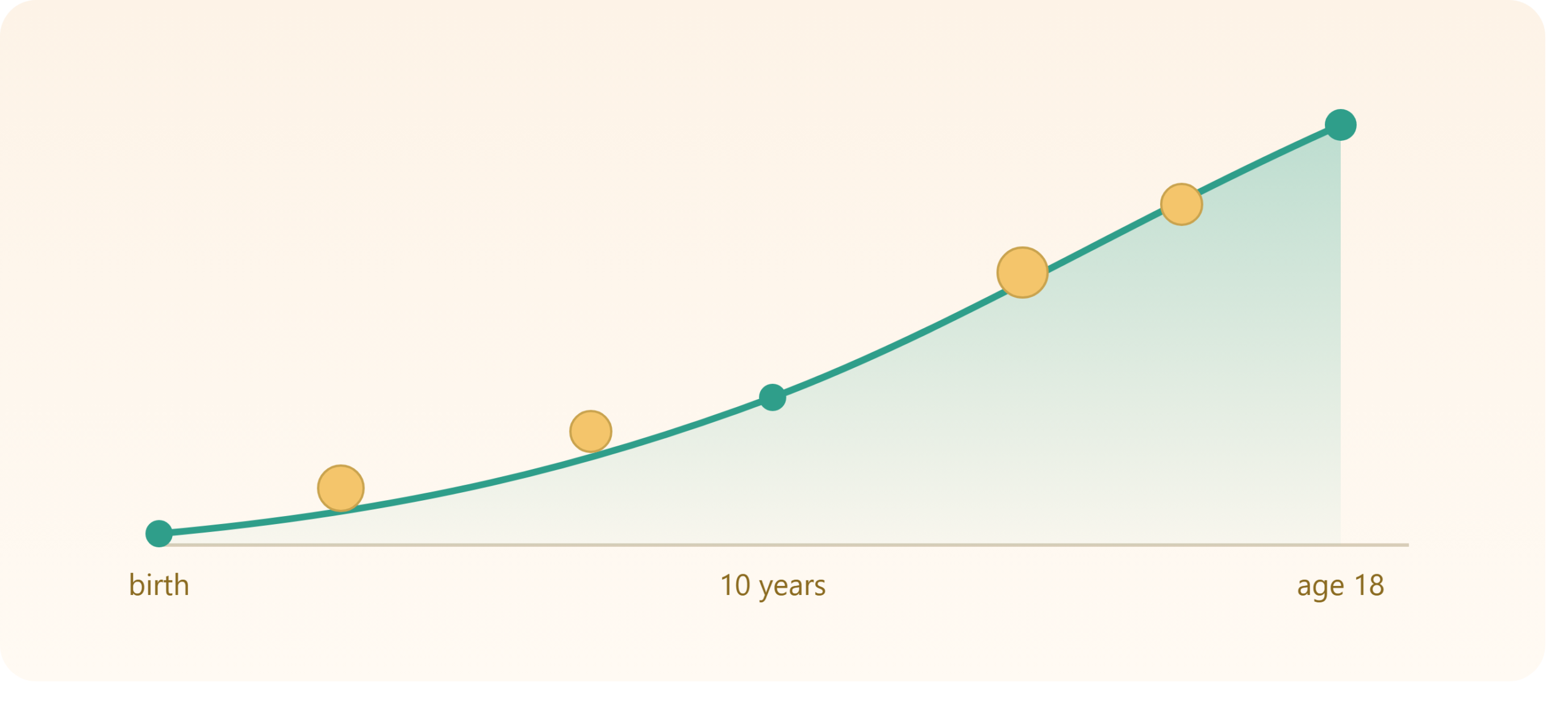

The Big Question: How Much Could This Actually Grow To?

This is where the marketing gets ahead of the math a little. Treasury officials have floated a headline number — that an account could be worth around $600,000 by retirement age, assuming historical stock market returns hold up and no further contributions are made beyond the initial $1,000.

Separate government analysis suggests a child born this year, with the maximum $5,000 contributed every single year until age 18, could have an account worth over $300,000 by adulthood — and potentially over $1 million by their late twenties under strong market conditions.

Worth remembering: these are projections based on past market performance, not guarantees. Markets don’t move in a straight line, and a downturn in any given decade could change these numbers significantly.

Trump Account vs. 529 Plan vs. Custodial Roth IRA

If you’re already saving for your child through other vehicles, here’s how a Trump Account stacks up:

| Feature | Trump Account | 529 Plan | Custodial Roth IRA |

|---|---|---|---|

| Purpose | Retirement | Education | Retirement |

| Requires earned income? | No | No | Yes |

| Access before 18 | No | Yes, for education | Contributions only |

| Withdrawal tax treatment | Ordinary income tax | Tax-free for education | Tax-free after 59½ |

| Annual contribution limit | $5,000 | Varies by state, much higher | Limited to child’s earned income |

If your priority is covering future tuition bills, a 529 plan still makes more sense. If your child already earns income (say, from a part-time job), a custodial Roth IRA may offer more flexibility and better tax treatment on withdrawals. The Trump Account fills a different gap: a no-effort way to start retirement savings before a child can even walk.

The Fine Print Parents Should Actually Read

A few details are easy to miss in the excitement:

- The money is locked up for a long time. Withdrawals generally aren’t possible until the child turns 18, and even then the funds convert into a traditional IRA — meaning early withdrawals could still trigger taxes and penalties depending on how they’re used.

- Withdrawals are taxed as ordinary income, not the lower long-term capital gains rate you’d get with a regular brokerage account.

- It could affect financial aid or benefits down the road. Questions remain about how account balances might interact with things like Pell Grant eligibility or SSI payments — guidance is still developing.

- Watch out for scams. The Treasury Department has explicitly warned that all official communication comes only from an official government email address, and that anyone calling or texting about your account should be treated as a scam attempt.

How to Open One

- Confirm your child has a Social Security number.

- Fill out IRS Form 4547, either directly with the IRS or through the official government portal.

- If applying for the $1,000 seed deposit, note that the person opening the account must be able to claim the child as a dependent for the child tax credit.

- Track your child’s account through the official government app or website — never through a link sent by text or email.

Bottom Line

Trump Accounts won’t solve today’s grocery bill or childcare costs, and they’re not a replacement for an education fund. But as a truly passive, no-cost way to give a child an 18-year head start on retirement savings, they’re a meaningful new tool in the family finance toolkit — especially for parents who can pair the free seed money with even modest annual contributions.

As with any new financial product, it’s worth talking to a tax professional or financial advisor before deciding how heavily to lean into one, especially if you’re weighing it against an existing 529 plan or custodial account.

This article is for informational purposes only and does not constitute financial or tax advice. Consult a licensed financial advisor before making investment decisions for your child.

{kind=link}