How to Get Out of Student Loan Default in 2026: A Complete Step-by-Step Guide

If you’ve received a notice that your student loans are in default — don’t panic. You have options. This guide breaks down exactly what default means, what happens next, and the three proven ways to get out of it in 2026.

The Student Loan Crisis of 2026: What’s Happening?

The numbers are staggering. In the first quarter of 2026 alone, 2.6 million Americans had their federal student loans transferred to the Department of Education’s Default Resolution Group. That’s on top of roughly 1 million defaults in late 2025 — and the crisis shows no sign of slowing.

Why now? Because pandemic-era protections that paused student loan collections have finally ended. Millions of borrowers who had been shielded for years are suddenly facing the full weight of their debt — many of them unprepared.

Key Statistics You Need to Know

- 2.6 million new defaults in Q1 2026

- $1.77 trillion total US student debt

- 91 points average credit score drop after default

- 39 years old is the average age of a newly defaulted borrower

What Exactly Is Student Loan Default?

A federal student loan enters default when you’ve missed payments for 270 days (about 9 months). Private student loans can go into default much faster — sometimes after just one missed payment, depending on your lender’s terms.

What happens when you default:

- Your entire loan balance becomes due immediately

- Your credit score drops by 50–100+ points

- The government can garnish your wages (up to 15% of disposable income)

- Your tax refund can be seized

- Federal benefits like Social Security can be offset

- You lose access to future federal financial aid

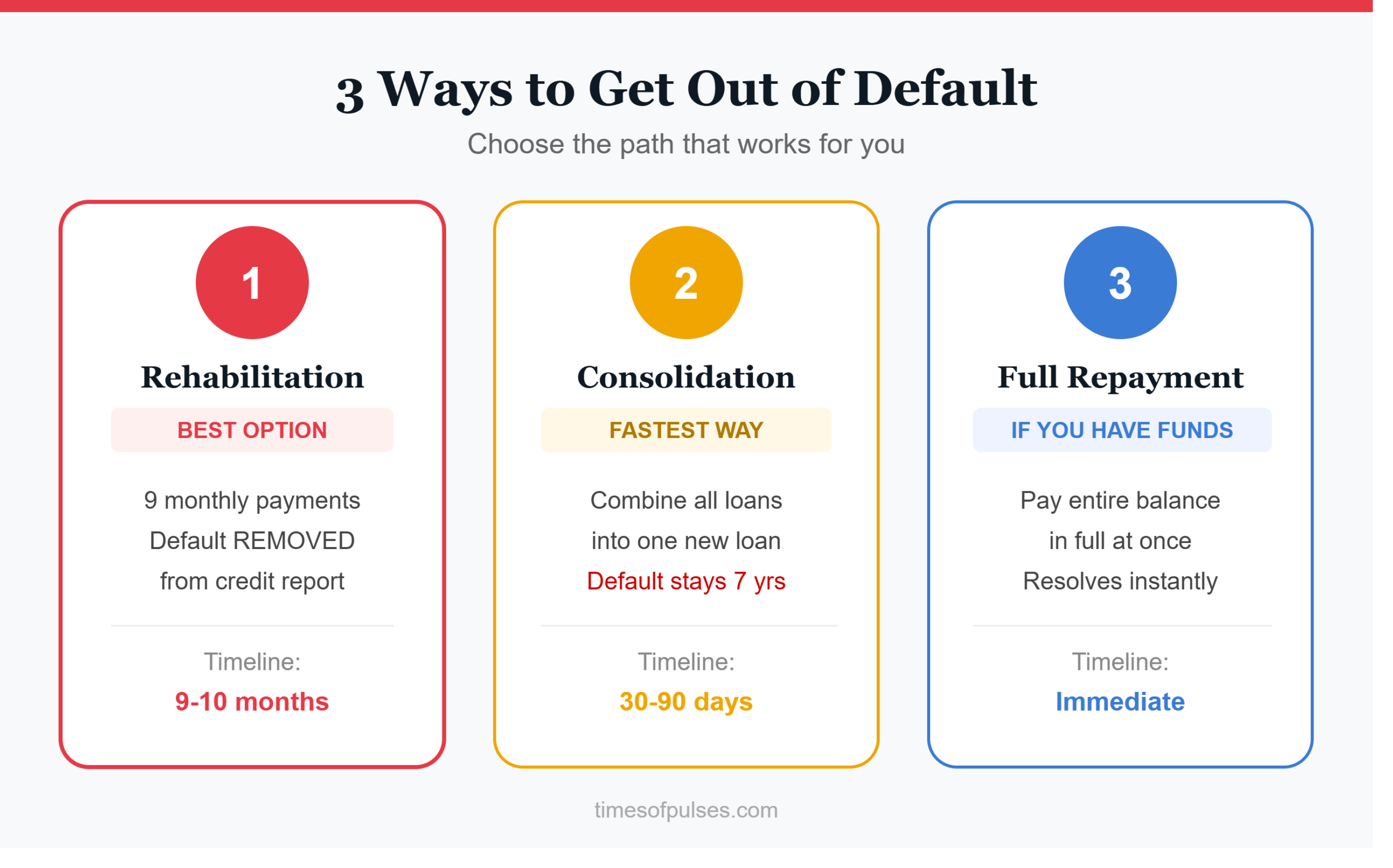

3 Ways to Get Out of Student Loan Default in 2026

The good news: the federal government offers three official pathways to resolve a defaulted student loan. Each has pros, cons, and different timelines. Here’s what you need to know.

Option 1 — Loan Rehabilitation (Best Option)

Loan rehabilitation is the most recommended option for most borrowers because it removes the default notation from your credit report entirely.

How it works:

- Contact your loan servicer or the Default Resolution Group

- Agree to make 9 voluntary, reasonable, and affordable monthly payments within a 10-month window

- Payments are calculated based on your income — they can be as low as $5/month if your income is very low

- After 9 on-time payments, your loan is rehabilitated and transferred back to a regular servicer

- The default record is removed from your credit history completely

Timeline: 9–10 months

Best for: Anyone who wants the default completely wiped from their credit report

Important Note: You can only rehabilitate a loan once. If you default again, this option is no longer available.

Option 2 — Loan Consolidation (Fastest Way Out)

Consolidation means combining your defaulted loan(s) into a new Direct Consolidation Loan. This pays off the old loan immediately, ending the default status — often within 30–90 days.

Two ways to qualify:

- Make 3 consecutive, voluntary, on-time monthly payments on the defaulted loan before consolidating, OR

- Agree to repay the consolidation loan under an income-driven repayment (IDR) plan

Timeline: 30–90 days

Best for: People who need to resolve default quickly

Important Note: The default notation stays on your credit report for 7 years unlike rehabilitation which removes it

Option 3 — Repayment in Full

If you’ve received a financial windfall — an inheritance, a bonus, or savings — you can pay the entire defaulted balance in full. This immediately resolves the default.

Timeline: Immediate

Best for: Borrowers who have the financial means to pay everything off

Rehabilitation vs. Consolidation: Which Is Better?

- Rehabilitation: Takes 9–10 months BUT removes default from credit report completely ✅

- Consolidation: Takes only 30–90 days BUT default stays on credit report for 7 years ❌

Bottom Line: For most borrowers, rehabilitation is the better long-term choice because it removes the default from your credit history. Choose consolidation only if speed is your top priority.

Warning — If You Don’t Act, Government Can:

- Garnish up to 15% of your disposable income every paycheck

- Seize your entire federal and state tax refund

- Offset your Social Security benefits

Don’t wait for a garnishment notice. Contact the Default Resolution Group now at 1-800-621-3115 to start the rehabilitation process.

How to Protect Your Credit Score After Default

The average credit score drop after student loan default is 91 points. Here’s what you can do right now to minimize the damage:

- Start rehabilitation immediately — wage garnishment stops after 5 on-time payments

- Pay all other bills on time — your payment history is 35% of your credit score

- Keep credit card balances low — ideally below 30% of your limit

- Don’t close old credit accounts — length of credit history matters

- Monitor your credit report at AnnualCreditReport.com (free, once per week)

- Dispute any errors on your credit report related to the default

Income-Driven Repayment: Your Safety Net Going Forward

Once you’re out of default, the most important thing is staying out. The best way to do that is to enroll in an Income-Driven Repayment (IDR) plan. Under IDR plans, your monthly payment is capped at a percentage of your discretionary income — typically 5% to 10%. If your income is low enough, your payment can literally be $0/month.

Current IDR options in 2026:

- SAVE Plan (Saving on a Valuable Education)

- Pay As You Earn (PAYE)

- Income-Based Repayment (IBR)

- Income-Contingent Repayment (ICR)

Frequently Asked Questions

How long does a student loan default stay on my credit report?

Seven years from the date of the first missed payment — unless you go through rehabilitation, which removes the default notation entirely.

Can I still get federal financial aid if I’m in default?

No. You must resolve your default before receiving any new federal grants or loans. This includes Pell Grants.

Will I go to jail for not paying student loans?

No. Student loan default is a civil matter, not a criminal one. You cannot be arrested for defaulting on student loans.

What if I can’t afford even the minimum rehabilitation payment?

Tell your loan servicer. Rehabilitation payments are based on income and can be as low as $5/month. There is always an option — you just have to ask.

Does student loan default affect my spouse?

Generally, no — unless you live in a community property state or your spouse co-signed the loan.

Final Thoughts

Student loan default feels overwhelming — but it is not a life sentence. Millions of Americans are in the same position in 2026, and the government has built real pathways to recovery. The most important thing you can do right now is stop ignoring it.

Pick up the phone. Call the Default Resolution Group. Start rehabilitation. Protect your wages, your tax refund, and your credit score — before collections resume.

You didn’t get into this situation overnight, and you won’t get out of it overnight either. But with the right plan and 9 months of consistent action, you can close this chapter for good.

Disclaimer: This article is for informational purposes only and does not constitute legal or financial advice. For personalized guidance, consult a certified student loan counselor or financial advisor.

{kind=link}